Different payment methods — the complete guide

Setting up a business may be both exciting and challenging, but there are important steps that cannot be missed. One of them is choosing payment methods to offer to clients. This decision may increase conversion rates, boost sales and help generate more revenue.

However, it may also have opposite effects if chosen without proper consideration.

Companies and third-party payment service providers must think about which payment methods are most appealing to the end-users and make sure these options are available when consumers get to the checkout.

This guide will explain what payment methods are, list the main forms of payment, review the most popular online payment methods and suggest how to choose the best payment methods for a business.

What is a payment method?

A payment method is a way to pay for goods or services. Payment options can differ depending on whether the business is based online or in a physical store.

In-store payment methods include cash, bank cards and paying with mobile devices. Online payment options cover card payments, bank transfers, e-wallets, and account-to-account (A2A) payments.

What are the main forms of payment?

There are two main forms of payment: in-store and online. Each of these forms covers various payment methods, such as cash, card payments, bank transfers, e-wallets, etc. Below is a list of the payment methods involved in each payment form:

In-store payment methods

In-store payment methods are used to pay for goods or services in physical stores. Merchants and other businesses often offer more than one payment method to suit the needs of their clients.

Cash payments

Cash was the most common form of payment for a long time. However, the global pandemic and other factors have reduced its popularity. While it’s still one of the most popular payment methods for physical stores, it has its drawbacks.

Advantages

- Widely used

- Available via ATMs or banks

- No acceptance charges

Disadvantages

- Security issues

- Inconvenient, as cash can take up much space and requires secure storage

- Exchanging different currencies is inconvenient for consumers

Credit or debit card payments

Many people own and use bank cards. Their usage varies between countries, but they’re one of the primary in-store payment methods. The new trends show that currently-used payment cards aren’t necessarily issued by banks. Non-banking companies now offer loans, Buy Now, Pay Later (BNPL) functionalities and other features.

Advantages

- One of the most popular payment methods

- Cards don’t take much space

Disadvantages

- Fraud risk

- Card payment acceptance charges are high

Options

The most popular card schemes worldwide are Visa, MasterCard and American Express.

Bank transfers

Manual bank transactions aren't the most convenient payment method for physical stores, but merchants often use them to avoid card processing fees. This payment method is often used by smaller merchants who wish to save on card transaction costs.

Advantages

- No card processing fees

- Quicker settlement time

Disadvantages

- Poor customer experience

- In some cases, the consumer may need to pay bank transfer fees

Mobile or Near Field Communication (NFC) payments

More and more stores use point-of-sale (POS) terminals to accept card or mobile payments. Mobile payments don't have to be done specifically by using Apple Pay or Google Pay and tokenized payment cards. There are also multiple platforms using QR code payments.

Advantages

- User-friendly

- Available to everyone with a smartphone

Disadvantages

- In most cases, mobile payments involve paying by card, which means merchants need to pay card fees

Online payment methods

When shopping online, consumers expect to be able to pay with their preferred payment options. Offering convenient payment methods can improve conversion rates, so providing the most popular methods and a convenient checkout flow are important for online businesses.

Debit, credit or prepaid cards

Since many people own bank cards, they also use them to pay for goods and services online. While in physical stores, consumers can use their cards with a chip and pin. Online, they’re required to enter their card number, expiry date and a CVV code.

Advantages

- Users can link their bank cards to various apps, which is convenient for quick purchases

Disadvantages

- Security issues

- Card processing fees

Options

Debit, credit, or prepaid cards for online purchases are mainly issued by the same providers as physical cards. The most popular card schemes are Visa, MasterCard and American Express.

Direct bank transfers

Consumers can receive an invoice via email and make a manual bank transfer to a service provider. The process is rather simple, but it may not be the most convenient payment method for online businesses because of the discontinuous checkout flow.

Advantages

- No card processing fees

- Quick settlement

Disadvantages

- Can cause high cart abandonment rate due to inconvenience

- Leaves space for human errors when manually entering recipient’s bank account information

E-wallets

Consumers can attach their bank cards to a digital wallet and use their mobile devices to pay for goods or services online. E-wallets as a payment method are pushing out the usage of credit cards, which is decreasing yearly.

Advantages

- User-friendly and convenient apps

- Available to everyone with a smartphone

Disadvantages

- Merchants may pay card processing fees

Options

Apple Pay, Google Pay, Samsung Pay and PayPal are among the most popular digital wallet services.

A2A payments

Account-to-account payments are safe and convenient for merchants and consumers. A2A enables paying directly from a bank account, bypassing card processing fees for businesses and improving security for consumers. If the bank allows instant or SEPA instant payments, A2A payments also enable instant fund transfers from the customer to the merchant.

Advantages

- No card processing fees

- Quick settlement

- Frictionless user checkout experience

Disadvantages

- Can take a few days to process the payment if consumer and merchant bank accounts are in different currencies

Options

kevin. offers account-to-account payments and an account linking feature, which make direct account payments quick and convenient for both merchants and their customers.

Cryptocurrencies

More and more online merchants are considering accepting cryptocurrencies as an online payment method. Crypto payments are considered to be more secure than traditional payment methods because they don’t require third-party verification, and no consumer data is stored in a centralised hub. However, accepting these payments is also risky because of their volatile value.

Advantages

- Lower risk of payment fraud compared to credit and debit cards

- Lower acceptance charges

Disadvantages

- High risk due to value unpredictability

Options

Bitcoin is one of the most popular cryptocurrencies. Other options include Ethereum, Tether, USD Coin, etc.

Most popular online payment methods

The most popular online payment methods vary by country. According to statistics, the most popular payment method among global consumers in 2021 was digital or mobile wallets. They made up 49% of e-commerce expenditure worldwide. The popularity of mobile wallets is set to rise to 53% by 2025.

Credit and debit cards were the second most popular online payment method in 2021 and made up 34% of global e-commerce transactions. Their popularity is expected to fall to 32% in 2025.

Bank transfers are the third most popular payment option, accounting for 7% of e-commerce spending. This payment method is primarily used in Europe.

The Central and Eastern Europe (CEE) region still tends to favour paying cash on delivery. For example, this payment method holds around 30% of the market share in the Czech Republic.

What are the alternative online payment methods?

Alternative payment methods are a way of paying for goods or services with other methods than cash or using the largest card schemes. By definition, the alternatives cover something other than the mainstream options. But when it comes to payments, in some markets, alternative payment methods are more popular than the mainstream ones.

The main alternative payment methods are:

Online banking

All payments made from a bank account are considered to be online banking payments. These payments don’t require entering bank card information and can be made directly from a bank account. One of the main advantages of this alternative payment method is the low payment acceptance costs for merchants.

Direct debits

Subscription-based businesses prefer direct debits because they are a great option for accepting recurring payments. Consumers consent to merchants automatically pulling the agreed payment amount from their bank account, which is convenient for both businesses and consumers.

Mobile payments

Mobile payments are made via a smartphone, using a mobile payment app, such as Samsung Pay, PayPal or others. Mobile payments can be made in-app, via a QR code, or even via SMS.

Digital wallets

Digital wallets enable users to store funds electronically. Users can top up their wallets via a bank transfer, mobile carrier or a bank card. E-wallets allow consumers to conveniently make online purchases, pay bills or transfer money to others.

Buy Now, Pay Later (BNPL) financing

The market sees an increasing focus on Buy Now, Pay Later services, which are a form of a short-term loan provided to the end user. BNPL enables consumers to get products and pay for them later or spread the cost over a period of time. Some of the most popular BNPL payment method providers charge no interest, which makes this payment option popular among consumers who don’t have credit cards.

Alternative payment methods are on the rise, especially after open banking paved the way for new companies offering innovative solutions to step into the market.

The most popular payment service providers (PSPs) offering alternative payment methods are:

- Google Pay (using tokenized Visa or MasterCard payment card)

- Apple Pay (using tokenized Visa or MasterCard payment card)

- Alipay

- PayPal

- Klarna

The popularity of alternative payment methods varies from country to country. Different payment service providers have settled into various markets, with Alipay taking 55% of the mobile payment market share in China and Klarna holding more than 50% of the global BNPL market.

What are the most secure online payment methods?

The most secure online payment methods are direct bank account payments, bank cards (credit and debit), and digital wallets. These are their main security features:

Bank account payments

Paying directly from your bank account is one of the most secure payment methods. This is partly due to the PSD2 security standards, including strong customer authentication (SCA), that ensure bank payments can only be initiated by identified users.

Bank cards

Credit and debit cards use a 3D secure protocol for online payment security. Cardholders receive a code via SMS or a mobile application that is used to authenticate the payer. This way, 3D secure reduces card payment fraud. However, card payment fraud is still a common issue.

Digital wallets

E-wallets such as Apple Pay or Google Pay allow paying for goods or services via a mobile device and a bank card connected to the device. With the appropriate security measures set on a mobile device, digital wallets are one of the most secure payment methods.

How to choose the best payment method for your businesses

When choosing payment methods for your business, you should consider a few factors and find the answer to the question of how your consumers prefer to pay. Most consumers will abandon their carts if they can’t find their preferred payment method at the checkout.

Here are the factors to consider when comparing the best online payment providers:

Price

Depending on the payment method, businesses can pay significant amounts for every transaction. For example, the largest card schemes may charge a percentage of the transaction and a fixed price per payment. This could amount to a large part of the total payment.

Features

Varying country coverage and bank account linking are some of the features that different services or payment gateways may offer. Consider what features would be most beneficial for your business.

Flexibility

How soon will the funds be deposited into your business account? What is the refund policy? If all these questions regarding flexibility are relevant to your business, find out the answers before committing to a payment service provider.

Security

Security is one of the most important factors to consider when choosing the best payment method. For example, in the case of payment fraud, who will be responsible for the damage: your company, or the payment service provider (PSP)?

What is the future of digital e-commerce payments?

Different sources predict various future scenarios, but most share one vision - digital payments will continue growing. The pandemic has already accelerated the growth of digital e-commerce payments, and they’re not stopping here.

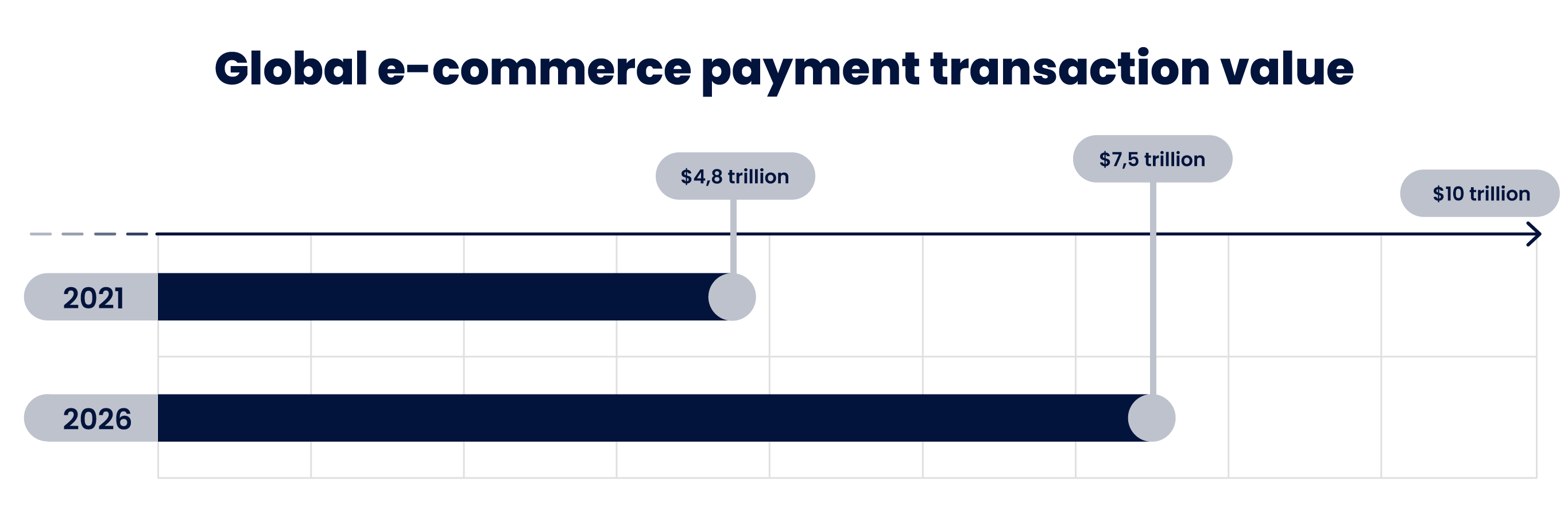

Juniper Research announced that the value of e-commerce payment transactions around the world will exceed $7.5 trillion by 2026. In 2021, its value was $4.8 trillion, which means a 55% growth rate over five years.

Digital payment service providers will have to find ways to meet the demand and offer payment methods that serve the needs of their customers. Open banking has already shifted the landscape of the payment industry by enabling innovations and creating a more competitive environment for traditional payment methods. To stay in the market, companies will need to address the shift in demand for payment methods.

How can kevin. help?

kevin. offers innovative payment methods with the highest security standards. Merchants and PSPs can utilise kevin. features to provide their clients with the benefits of open banking.

With kevin., companies and PSPs can integrate advanced A2A payments that cover most EU and EEA countries and significantly reduce transaction costs. To learn more about what kevin. has to offer, get in touch with our team.